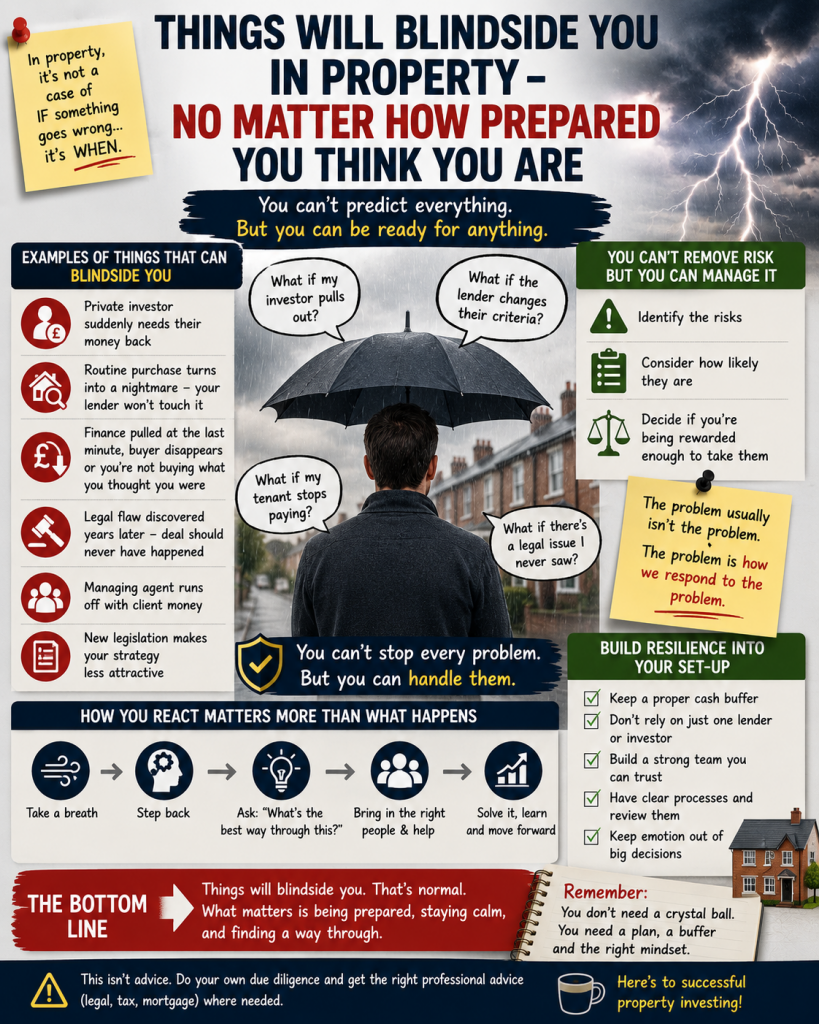

Things will blindside you in property, no matter how prepared you think you are.

That’s not pessimism, that’s just life.

It happens in business, it happens in relationships, and it definitely happens in property.

You can plan, stress test, spreadsheet and scenario-plan all you like — at some point something will happen that you couldn’t reasonably have seen coming.

In property that might look like:

- Your private investor suddenly needing their money back because they have a crisis.

- A “routine” purchase turning into a nightmare because, thanks to a technicality you’d never heard of, your buy-to-let lender won’t touch the deal.

- You’re poised to exchange and complete, and at the last minute the finance is pulled, or your buyer disappears, or it turns out you’re not actually buying what you thought you were buying.

There are a million and one ways things can go sideways.

You won’t catch them all in advance.

The deal that should never have happened

Here’s a real one from my own portfolio.

I bought a property. I bought it with a mortgage. I used a solicitor. My solicitor liaised with the legal department at the mortgage company.

Everyone was happy. The mortgage completed, the lender was paid, the tenant moved in.

For about four years, life was completely uneventful.

Then I decided to sell.

I put the property on the market, received an offer, agreed a sale. All very normal.

It was only when the buyer’s solicitor started digging a bit deeper that we discovered there was a significant legal flaw which meant I shouldn’t have been able to buy the property in the first place — and I certainly shouldn’t have been able to obtain a mortgage on it.

Unpicking that mess took about a year.

I lost the sale.

And in the meantime my solicitor had retired, his firm had pulled down the shutters, and made it abundantly clear they weren’t going to help or offer compensation.

Totally crazy situation.

And at the time, totally unpredictable.

Could I have done more due diligence?

To be honest, I don’t think I could have in this situation.

And realistically, if the lender’s legal team and my own solicitor all signed it off, most investors would have assumed it was all fine as well.

So if this sort of thing can happen… should we just avoid property altogether?

No. Of course not.

But we do need to go in with our eyes open and accept that stuff happens.

Every time you buy a property, there is risk. Full stop.

I’ve been involved in property for over 40 years, and I’ve lost count of the number of people who have told me that they wanted a risk-free way of investing in property, and so asked me how to do it.

That’s never going to happen.

You can manage risk.

You can reduce risk.

You can price in risk.

But you can’t eliminate it.

If anyone ever finds a way to make property investing, or any other type of investing for that matter, completely risk-free, please let me know. If we can bottle it, we’ll make a fortune together.

What you can do, as part of your due diligence, is:

- think about the types of risk,

- consider how likely they are to show up during your ownership,

- and decide if you’re being rewarded enough to take them.

Predictably unpredictable problems

There are problems which are predictably unpredictable.

For example, if you buy a buy-to-let, it is predictable that at some point the boiler will die.

You don’t know when — next month, three years from now, ten years from now — but if you own the property long enough, you know it will happen.

On that basis you can prepare.

Put aside a little of the rent each month to cover those predictably unpredictable repairs. Roof leaks, boilers, white goods — none of this is truly unexpected. We know it will happen, but we just don’t know when.

Inconvenient, yes.

Unexpected, no.

That’s the first level of defence: assume the boring stuff will go wrong and save for it.

Then there’s the stuff you really can’t predict

But there’s another category: things that are genuinely unpredictable and largely out of your control.

- Lenders suddenly changing criteria halfway through a purchase.

- New legislation that makes your carefully chosen strategy less attractive.

- A managing agent running off with client money.

- Title issues or historic legal mistakes, like in my example.

- A tenant’s personal disaster that turns into your arrears problem.

You can’t spreadsheet all of that away.

Somebody far cleverer than me — and I can’t remember who, so they probably won’t mind me butchering their quote — once said something along the lines of this:

The problem usually isn’t the problem.

The problem is how we respond to the problem.

That’s clunky philosophy, but quite good property investing.

How you react matters more than what happens

So the key thing isn’t, “How do I avoid anything bad ever happening?”

The key thing is this:

When something unpredictable happens, do I fall apart, or do I solve it?

If we’re not careful, we can easily slip into victim mode — blaming the universe, the government, the seller, the tenant, the bank, Mercury being in retrograde…

Much more useful is to:

- take a breath,

- step back,

- and ask, “Right. Given where we are, what’s the best way through this?”

It very often means bringing in people, organisations, processes and procedures that can help you untangle the mess.

That might mean:

- speaking to a good solicitor, or another one if the first is useless,

- talking to your broker about alternative lenders or a different product,

- negotiating with a buyer, seller or tenant instead of going straight to war,

- changing strategy — for example, switching from selling to refinancing and holding.

And it may well mean we need to look at our mindset to make sure we give ourselves the best possible chance of resolving it, without going to pieces and losing the plot.

Practical ways to prepare, without going paranoid

You can’t predict the exact problems, but you can build a bit of resilience into your set-up.

A few ideas:

- Keep a proper buffer.

Not just for boilers and paint, but for voids, legal fees, surprise lender requirements, unexpected tax bills. A few months’ rent per property in reserve makes you much harder to knock over. - Don’t rely on just one lender or one investor.

If a single private investor or bank can stop your whole business overnight, that’s a risk in itself. - Build a team you can lean on.

A decent broker, a switched-on solicitor, a good accountant, and at least one local agent who will tell you the truth — not just what you want to hear. - Write things down.

Simple processes for how you buy, refurb, let, manage, and exit. When something goes wrong, tweak the process so you’re less exposed next time. - Keep emotion out of decisions.

Problems feel personal. But if you can treat them as puzzles rather than personal attacks, you’ll usually make better choices.

It’s very rare that an event or problem is truly terminal.

But it’s often the case that you need to be clear-headed, strong and persistent to find a way through.

Final thought

So no, this doesn’t mean “never invest in property”.

It means:

- accept that things will blindside you,

- prepare for the predictable stuff,

- and practice staying calm and solution-focused when the unpredictable turns up.

As always, this isn’t advice.

You still need to do your own due diligence, run your own numbers, and, where needed, take proper legal, tax and mortgage advice.

Here’s to successful property investing.

Peter Jones

Author, property investor and ex-Chartered Surveyor

PS. By the way, if you’d like a deeper dive into property investing based on the real-life experience of an investor who has built a substantial multi-property portfolio, my popular e-book, The Successful Property Investor’s Strategy Workshop, explains how I built my own portfolio from scratch and the principles that can help you do the same.

PS. By the way, if you’d like a deeper dive into property investing based on the real-life experience of an investor who has built a substantial multi-property portfolio, my popular e-book, The Successful Property Investor’s Strategy Workshop, explains how I built my own portfolio from scratch and the principles that can help you do the same.

For more details please click here: https://thepropertyteacher.co.uk/the-successful-property-investors-strategy-workshop